Life Sciences

EY Eyes Comeback for Biopharma M&A

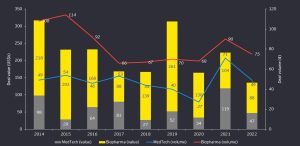

EY noted that the total value of biopharma M&A in 2022 was $88 billion, down 15% from $104 billion in 2021. The $88 billion accounted for most of the…

A recent trickle of mergers and acquisitions (M&A) announcements in the billion-dollar-and-up range suggests that biopharma may be ready to resume dealmaking this year—although the value and number of deals isn’t expected to return to the highs seen just before the pandemic.

2022 ended with a handful of 10- and 11-figure M&A deals, led by Amgen’s $27.8 billion buyout of Horizon Therapeutics, announced December 13. The dealmaking continued into January with three buyouts announced on the first day of the recent J.P. Morgan Healthcare Conference: AstraZeneca agreed to acquire CinCor Pharma for up to $1.8 billion, while Chiesi Farmaceutici agreed to shell out up to $1.48 billion cash for Amryt, and Ipsen Group said it will purchase Albireo Pharma for $952 million-plus.

EY—the professional services firm originally known as Ernst & Young—recently noted that the total value of biopharma M&A in 2022 was $88 billion, down 15% from $104 billion in 2021 [See Chart]. The $88 billion accounted for most of the $135 billion in 124 deals in the life sciences. That $135 billion figure is less than half the record-high $313 billion recorded in 2019, including $261 billion in 70 biopharma deals.

The number of biopharma deals fell 17% to 75 deals from 90. EY’s numbers include only deals greater than $100 million. The other 49 deals totaling $47 million consisted of transactions in “medtech,” which includes diagnostics developers and companies specializing in “virtual health” such as telemedicine.

“We expect this to be a more active year as the sentiment starts to normalize a little bit,” Subin Baral, EY Global Life Sciences Deals Leader, told GEN Edge.

Baral is not alone in foreseeing a comeback for biopharma M&A.

John Newman, PhD, an analyst with Canaccord Genuity, predicted last week in a research note that biopharma companies will pursue a growing number of smaller cash deals in the range of $1 billion to $10 billion this year. He said rising interest rates are discouraging companies from taking on larger blockbuster deals that require buyers to take on larger sums of debt.

“We look for narrowing credit spreads and lower interest rates to encourage larger M&A ($50 billion and more) deals. We do not anticipate many $50B+ deals that could move the XBI +5%,” Newman said. (XBI is the SPDR S&P Biotech Electronic Transfer Fund, one of several large ETFs whose fluctuations reflect investor enthusiasm for biopharma stock.)

Newman added: “We continue to expect a biotech swell in 2023 that may become an M&A wave if credit conditions improve.”

Foreseeing larger deals than Newman and Canaccord Genuity is PwC, which in a commentary this month predicted: “Biotech deals in the $5–15 billion range will be prevalent and will require a different set of strategies and market-leading capabilities across the M&A cycle.”

Those capabilities include leadership within a specific therapeutic category, for which companies will have to buy and sell assets: “Prepared management teams that divest businesses that are subscale while doubling down on areas where leadership position and the right to win is tangible, may be positioned to deliver superior returns,” Glenn Hunzinger, PwC’s U.S. Pharma & Life Science Leader, and colleagues asserted.

The Right deals

Rising interest and narrowing credit partially explain the drop-off in deals during 2022, EY’s Baral said. Another reason was sellers adjusting to the drop in deal valuations that resulted from the decline of the markets which started late in 2021.

“It took a little bit longer to realize the reality of the market conditions on the seller side. But on the buyer side, the deals that they were looking at were not just simply a valuation issue. They were looking at the quality of the assets. And you can see that the quality deals—the right deals, as we call them—are still getting done,” Baral said.

The right deals, according to Baral, are those in which buyers have found takeover targets with a strong, credible management team, solid clinical data, and a clear therapeutic focus.

“Rare disease and oncology assets are still dominating the deal making, particularly oncology because your addressable market continues to grow,” Baral said. “Unfortunately, what that means is the patient population is growing too, so there’s this increased unmet need for that portfolio of assets.”

Several of 2022’s largest M&A deals fit into that “right” category, Baral said—including Amgen-Horizon, Pfizer’s $11.6-billion purchase of Biohaven Pharmaceuticals and the $6.7-billion purchase of Arena Pharmaceuticals (completed in March 2022); and Bristol-Myers Squibb’s $4.1-billion buyout of Turning Point Therapeutics.

“Quality companies are still getting funded one way or the other. So, while the valuation dropped, people were all expecting a flurry of deals because they are still companies with a shorter runway of cash that will be running to do deals. But that really didn’t happen from a buyer perspective,” Baral said. “The market moved a little bit from what was a seller’s market for a long time, to what we would like to think of as the pendulum swinging towards a buyers’ market.”

Most biopharma M&A deals, he said, will be “bolt-on” acquisitions in which a buyer aims to fill a gap in its clinical pipeline or portfolio of marketed drugs through purchases that account for less than 25% of a buyer’s market capitalization.

Baral noted that a growing number of biopharma buyers are acquiring companies with which they have partnered for several years on drug discovery and/or development collaborations. Pfizer acquired BioHaven six months after agreeing to pay the company up to $1.24 billion to commercialize rimegepant outside the U.S., where the migraine drug is marketed as Nurtec® ODT.

“There were already some kind of relationships there before these deals actually happened. But that also gives an indication that there are some insights to these targets ahead of time for these companies to feel increasingly comfortable, and pay the valuation that they’re paying for them,” Baral said.

$1.4 Trillion available

Baral sees several reasons for increased M&A activity in 2023. First, the 25 biopharma giants analyzed by EY had $1.427 trillion available as of November 30, 2022, for M&A in “firepower”—which EY defines as a company’s capacity to carry out M&A deals based on the strength of its balance sheet, specifically the amount of capital available for M&A deals from sources that include cash and equivalents, existing debt, and market cap.

That firepower is up 11% from 2021, and surpasses the previous record of $1.22 trillion in 2014, the first year that EY measured the available M&A capital of large biopharmas.

Unlike recent years, Baral said, biopharma giants are more likely to deploy that capital on M&A this year to close the “growth gap” expected to occur over the next five years as numerous blockbuster drugs lose patent exclusivity and face new competition from lower-cost generic drugs and biosimilars.

“There is not enough R&D in their pipeline to replenish a lot of their revenue. And this growth gap is coming between 2024 and 2026. So, they don’t have a long runway to watch and stay on the sidelines,” Baral said.

This explains buyers’ interest in replenishing pipelines with new and innovative treatments from smaller biopharmas, he continued. Many smaller biopharmas are open to being acquired because declining valuations and limited cash runways have increased investor pressure on them to exit via M&A. The decline of the capital markets has touched off dramatic slowdowns in two avenues through which biopharmas have gone public in recent years—initial public offerings (IPOs) and special purpose acquisition companies (SPACs).

EY recorded just 17 IPOs being priced in the U.S. and Europe, down 89% from 158 a year earlier. The largest IPO of 2022 was Prime Medicine’s initial offering, which raised $180.3 million in net proceeds for the developer of a “search and replace” gene editing platform.

Another 12 biopharmas agreed to SPAC mergers with blank-check companies, according to EY, with the largest announced transaction (yet to close at deadline) being the planned $899 million merger of cancer drug developer Apollomics with Maxpro Capital Acquisition.

“For the smaller players, the target biotech companies, their alternate source of access to capital pathways such as IPOs and SPACs is shutting down on them. So how would the biotech companies continue to fund themselves? Those with quality assets are still getting funded through venture capital or other forms of capital,” Baral said. “But in general, there is not a lot of appetite for the biotech that is taking that risk.

Figures from EY show a 37% year-to-year decline in the total value of U.S. and European VC deals, to $16.88 billion in 2022 from $26.62 billion in 2021. Late-stage financing rounds accounted for just 31% of last year’s VC deals, down from 34% in 2021 and 58% in 2012. The number of VC deals in the U.S. and Europe fell 18%, to 761 last year from 930 in 2021.

The decline in VC financing helps explain why many smaller biopharmas are operating with cash “runways” of less than 12 months. “Depending on the robustness of their data, their therapeutic area, and their management, there will be a natural attrition. Some of these companies will just have to wind down,” Baral added.

M&A headwinds

Baral also acknowledged some headwinds that are likely to dampen the pace of M&A activity. In addition to rising interest rates and inflation increasing the cost of capital, valuations remain high for the most sought-after drugs, platforms, and other assets—a result of growing and continuing innovation.

Another headwind is growing regulatory scrutiny of the largest deals. Illumina’s $8 billion purchase of cancer blood test developer Grail has faced more than two years of challenges from the U.S. Federal Trade Commission and especially the European Commission—while Congress acted last year to begin curbing the price of prescription drugs and insulin through the “Inflation Reduction Act.”

Those headwinds may prompt many companies to place greater strategic priority on collaborations and partnerships instead of M&A, Baral predicted, since they offer buyers early access to newer technologies before deciding whether to invest more capital through a merger or acquisition.

“Early-stage collaboration, early minority-stake investment becomes increasingly important, and it has been a cornerstone for early access to these technologies for the industry for a long, long time, and that is not changing any time soon,” Baral said. “On the other hand, even on the therapeutic area side, early-stage development is still expensive to do in-house for the large biopharma companies because of their cost structure.

“So, it is efficient cost-wise and speed-wise to buy these assets when they reach a certain point, which is probably at Phase II onward, and then you can pull the trigger on acquisitions if needed,” he added.

The post EY Eyes Comeback for Biopharma M&A appeared first on GEN – Genetic Engineering and Biotechnology News.

diagnostics

therapeutics

biosimilars

gene editing

pharmaceuticals

biotech

pharma

life sciences

healthcare

telemedicine

medicine

prescription

vc

venture capital

markets

fund

buy

sell

Wittiest stocks:: Avalo Therapeutics Inc (NASDAQ:AVTX 0.00%), Nokia Corp ADR (NYSE:NOK 0.90%)

There are two main reasons why moving averages are useful in forex trading: moving averages help traders define trend recognize changes in trend. Now well…

Spellbinding stocks: LumiraDx Limited (NASDAQ:LMDX 4.62%), Transocean Ltd (NYSE:RIG -2.67%)

There are two main reasons why moving averages are useful in forex trading: moving averages help traders define trend recognize changes in trend. Now well…

Asian Fund for Cancer Research announces Degron Therapeutics as the 2023 BRACE Award Venture Competition Winner

The Asian Fund for Cancer Research (AFCR) is pleased to announce that Degron Therapeutics was selected as the winner of the 2023 BRACE Award Venture Competition….